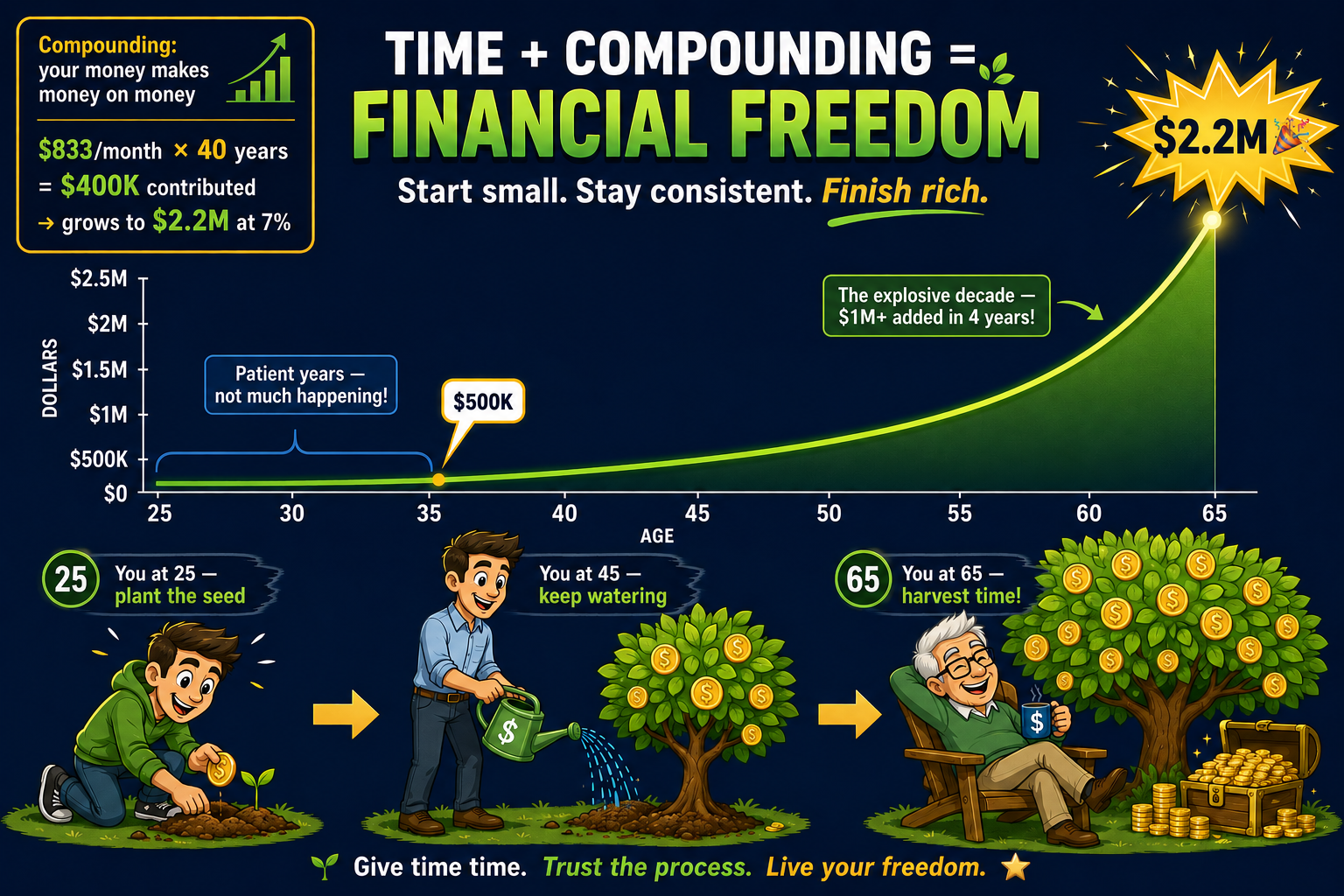

For Ages 25–40 · Accumulation Phase

GROW

EARLY.

RETIRE

BIG.

If You Start at 25 vs 35

$0

Projected 401(k) at age 65 · $833/mo ($10K/yr) · 7% avg return

💚 Start at 25 (40 yrs)

$2,187,000

🟡 Start at 35 (30 yrs)

$1,017,000

⚡ 10-year cost of waiting

-$1,170,000

The single biggest advantage you have over every older investor is time. Learn how to save smarter, invest wisely, and watch compounding do the heavy lifting.